New Tax Residency Rules in UAE: What You Need to Know

The United Arab Emirates (UAE) is a tax-friendly country with a relatively simple tax system. There is no personal income tax or capital gains tax. However, there are some taxes that apply to businesses and individuals, such as value-added tax (VAT), customs duties, and stamp duty and corporate tax.

One of the most important aspects of the UAE tax system is the definition of tax residency. Tax residency determines whether an individual or entity is liable to pay tax in the UAE. The UAE tax authorities use a combination of factors to determine tax residency, including the following:

- Physical presence: The number of days an individual spends in the UAE each year.

- Center of vital interests: Where an individual’s personal and financial interests are centered.

- Citizenship: Whether an individual is a UAE citizen or national of another country.

New Tax Residency Rules in UAE

On September 9, 2022, the UAE Cabinet of Ministers issued Decision No. 85 of 2022, which introduced new criteria for determining tax residency status in the UAE. The new criteria will replace the existing system of determining tax residency based on the number of days an individual spends in the UAE.

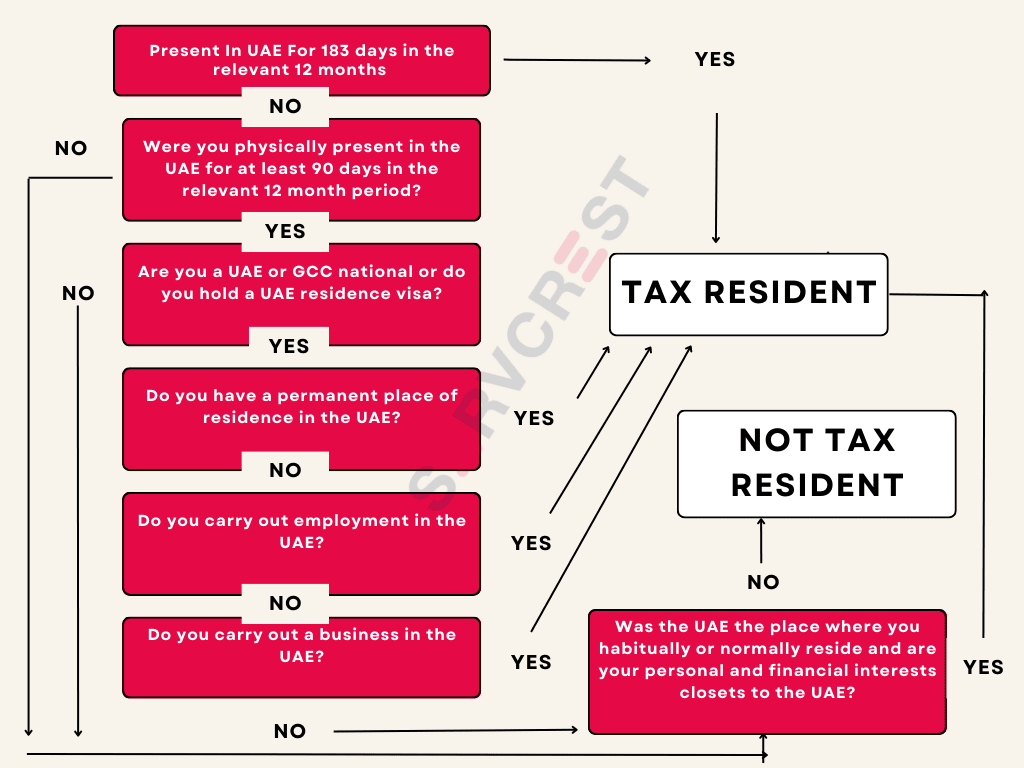

Under the new criteria, an individual will be considered a tax resident of the UAE if they meet any one of the following conditions:

- They spend at least 183 days in the UAE in a calendar year, whether consecutive or not.

- Their place of habitual residence is in the UAE, which means that they have a permanent home in the UAE that they regularly use for their personal or family purposes.

- They have an active UAE residence visa, which allows them to reside in the UAE for a period of at least 6 months in a year.

In addition to these three criteria, the new rules also provide for a 90-day rule. Under this rule, an individual may still be considered a tax resident of the UAE even if they do not meet any of the other three criteria, if they are not considered a tax resident in any other jurisdiction and they spend at least 90 days in the UAE in the calendar year.

The 90-Day Rule

The 90-day rule is particularly significant, as it provides greater flexibility in determining tax residency in the UAE and recognizes the diverse ways in which individuals may have ties to the country.

For example, an individual who spends less than 183 days in the UAE in a calendar year and does not have a permanent home or active residence visa in the UAE may still be considered a tax resident if they spend at least 90 days in the country and are not tax residents in any other country.

The 90-day rule is also important for individuals who frequently travel to the UAE for business or have family ties in the country. These individuals may now be considered tax residents of the UAE even if they do not spend the majority of their time in the country.

Impact of the New Tax Residency Rules in UAE

It is evident that the UAE has considered tax residency requirements per the global parameters and has realigned its position to provide a pragmatic approach. The revision addresses several gaps that existed under the previous regulations and practices of the Federal Tax Authority (FTA).

The UAE has double taxation treaties and bilateral agreements with 123 countries. These references the UAE’s domestic laws and are crucial in determining an individual’s tax residency status.

Eligible UAE residents can apply to the FTA to obtain Tax Residence Certificate (TRC), enabling them to further apply for tax relief, or claim benefits in a different jurisdiction under the applicable tax treaty.

Applicants meeting the 183+ or 90+ criteria and related objective conditions should be able to obtain a TRC with relative ease. Applications of those not meeting any of the day counting test, on the other hand, will be subject to discretionary interpretation by the FTA.

In this regards, evidence supporting documents that the UAE is the applicant’s principal place of residence AND centre of financial and personal interests will be key.

Conclusion

The introduction of the new tax residency rules in UAE is a significant development in the UAE tax system. The new criteria provide greater flexibility in determining tax residency and recognize the diverse ways in which individuals and entities may have ties to the country. The new criteria will also help to ensure that the UAE tax system remains competitive and attractive for individuals and businesses.

Additional Information

Here are some additional things to keep in mind about the New Tax Residency Rules in UAE

- The new criteria apply to both individuals and legal entities.

- The new criteria took effect from March 1, 2023.

- Individuals who are currently classified as non-residents for tax purposes but who meet any of the new criteria will be considered residents from March 1, 2023.

Individuals who are unsure about their tax residency status should consult with a tax advisor.

Meaning of key terms used in the definition of New Tax Residency Rules In UAE for individuals

What does the new UAE Tax Resident definition mean for individuals?

- The introduction of the new UAE tax residency criteria for individuals does not mean individuals will be subject to personal income tax in the UAE.

- The UAE does not levy any personal income tax on the employment or other personal income of individuals. As such, where an individual meets the above criteria to be considered a UAE Tax Resident, they would generally not be subject to taxation in the UAE on their personal income.

- The new Tax Resident definition gives additional clarity to individuals in respect of their UAE tax residency position under bilateral tax agreements the UAE has entered into with other territories, many of which make reference to the domestic laws of the UAE for determining whether a person is a resident of the UAE for purposes of the treaty.

- The Decision does not negate the fact that the UAE Corporate Tax Law will treat foreign natural persons conducting business in the UAE as a “Resident Person” (as defined in the Corporate Tax Law) when it comes to determining whether the person’s business income is taxable in the UAE. This Corporate Tax Law concept is unrelated to whether the natural person themselves is considered Tax Resident in the UAE for other tax purposes.

What counts as a day of presence in the UAE?

- In determining whether the individual has met the 183 or 90 day thresholds for a continuous 12 month period, all days or parts of a day on which the individual was physically present in the UAE will be counted. This straightforward rule will makes it simple for individuals to track their UAE days. Days spent in the UAE do not need to be consecutive.

Days spent in the UAE due to exceptional circumstances

- Individuals may choose to disregard from the day count, any days on which their presence in the UAE was due to exceptional circumstances.

- An exceptional circumstance is an event or situation outside of the individual’s control, which could not have reasonably been anticipated or prevented and which stops the individual from leaving the UAE when they originally planned

Permanent Place of Residence

- A Permanent Place of Residence is a furnished house, apartment, room or other form of dwelling place.

- The residence must be continuously available to the individual and occupied by them on a regular basis with some degree of permanency and stability.

- The individual does not need to own the residence – it can be rented or otherwise occupied by them.

When is an individual carrying on an employment in the UAE?

- An individual is carrying out an employment if they are party to an employment contract with an employer, which is incorporated or otherwise formed or recognised in the UAE.

- Certain other employment-like arrangements will also qualify, provided all or substantially all of the individual’s income for their labour carried out in the UAE is derived from one party.

- The employment can be limited or unlimited and the work may be carried out on a full time or part time basis. Voluntary roles will not be classed as employment.

When is an individual carrying on a business in the UAE?

- An individual will be considered to be conducting a business if they carry out any activity regularly, on an ongoing and independent basis, e.g. industrial, commercial, agricultural, professional, vocational, service or excavation activities or activity related to the use of tangible or intangible properties.

Usual or Primary Place of Residence and Centre of Financial and Personal Interests

- Individuals may also be tax resident in the UAE if this is the place where they normally live as part of their settled routine and where they spend most of their time as compared to any other jurisdiction.

- The UAE must also be the place where their centre of financial and personal interests is the closest or of the greatest significance to them. This takes into account their occupation or place of business, their family and social relations, cultural or other activities and any other relevant facts.

New Tax Residency Rules in UAE for Companies

The new definition of juridical person generally refers to an entity established or otherwise recognised under the laws and regulations of the UAE, or under the laws of a foreign jurisdiction, that has a legal personality separate from its founders, owners and directors.

Examples of UAE juridical persons include a limited liability company, a foundation, a public or private joint stock company, and other entity forms that have separate legal personality under the applicable UAE mainland legislation or the regulations of a free zone

A company is considered to be a Tax Resident of the UAE if:

- it is incorporated or otherwise formed or recognised in the UAE; or

- it is otherwise considered a Tax Resident of the UAE under the applicable legislation in the UAE.

UAE branches of a domestic or a foreign juridical person are an extension of their “parent” or “head office” and are not considered separate juridical persons. A branch of a foreign juridical person registered in the UAE would therefore generally not be considered a Tax Resident of the UAE.

What does the New Tax Residency Rules in UAE mean for companies?

- Companies which are considered to be UAE Tax Resident may be liable to Corporate Tax in the UAE under the Corporate Tax Law.

- The Cabinet Decision refers to the “applicable Tax Law” (the Corporate Tax Law) to determine whether a foreign juridical person is Tax Resident. For any other person, the UAE tax residency requirements are set out in Cabinet of Ministers Decision No. 85 for 2022